The Art of Micro SaaS Valuation

Micro SaaS marketplaces are all fine and dandy, but what is a founder to expect when he puts up his startup for sale? Should he jump on the first offer or spend months waiting for an offer he won't be able to refuse? Making an informed decision is impossible without first knowing the value of the asset at hand.

This is where things get a little bit tricky. A micro SaaS is, by definition, a bootstrapped endeavor and it shuns outside funding for the purpose of remaining independent. Hence, there is no prior investment. To make it worse, most micro SaaS companies are listed for sale at the idea stage, with no revenue to speak of. With no quantitative data available to serve as a basis for valuation, we are wandering into the field of prophecy if we want to put a price tag on a project.

Putting a price on potential

Somebody trying to appraise a micro SaaS business is in the same position as the general manager (GM) of an NBA team, weighing if he should offer a nine-figure contract extension to a player on a rookie contract. During his 4-year long rookie contract, a player is bound to have many ups and downs, run into the infamous "rookie wall," and get injured, which combine to limit the body of work a GM can use to gauge the player's potential. The glimpses of greatness might be there: A few nights of scoring outbursts here and some defensive stops there. However, the player most likely has weaknesses in his game, too, or maybe even injury concerns. Does he have the work ethic to improve his game? Can he stay healthy?

Giving a big contract to a player who later turns out to be a flop can cripple a franchise for years to come. On the other hand, if the GM lets the player walk, there is always the risk of him turning into a star one day, leaving the GM with the guilty conscience of a decision-maker who discovered a diamond in the rough but gave it away. Long story short, assessing potential is an art unto itself.

This applies to the micro SaaS segment, too. Whether you are a seller or a buyer in the market, you want to get a good deal. Learning that you could have gotten much more than you did for your startup or that you paid more than you should as a buyer stings. Even a ballpark figure can help start off the negotiations on the right foot. Luckily, angel investors have been dealing with the problem of appraising pre-money (i.e., a company that has never received outside funding before) pre-revenue startups. Their methods can be used to determine the valuations of micro SaaS projects.

The Berkus Method

Dave Berkus is an early-stage venture capitalist who had first-hand experience with the pain of putting a price on a pre-revenue startup. Unable to find a way, he decided to make one for himself, as one North African general had once said. Berkus designed a technique to help evaluate early-stage startups without financials.

Early-stage startups operate in a sea of uncertainty and risks. Berkus concluded that any steps taken to mitigate major risk factors should reflect as a premium on the valuation of a startup. He defined four pre-revenue risk-mitigating factors and an additional post-revenue one:

- Sound Idea (basic value)

- Prototype (reduces technology risk)

- Quality Management Team (reduces execution risk)

- Strategic Relationships (reduces market risk)

- Product Rollout or Sales (reduces production risk)

Berkus hypothesized that the presence of each risk-mitigating factor added half a million dollars to the startup's valuation. So, a startup that has ticked off the first four items would be valued at $2 million. While developing this framework, Berkus took care that the startup would be valued at a low enough price to give investors enough room to achieve at least a 10X return on their investments. Therefore, investors could expect the hypothetical startup above to reach a valuation of $20 million at the end of its fifth year.

The Berkus Method was developed in the mid-1990's, so it needed revisioning more than once during the past three decades. Berkus adjusted the method in a way that would reflect the sharp increase in tech startup valuations over time. He also acknowledged that users should allow for the influence geographical differences had on valuations. So, a startup based in Silicon Valley and focusing on a trendy problem like "big data" could justify a $1.5 million per element, while the price tag would be significantly lower for startups operating out of a Midwestern city.

In addition to providing founders and investors with a valuation figure, the Berkus method also establishes a direct link between the risks surrounding a startup and its appeal in the eyes of investors. Founders would benefit immensely from incorporating this approach into how they run their startups.

Scorecard Valuation Method

Another methodology used to assess the value of a pre-money startup is the Scorecard Valuation Method, which was devised by angel investor Bill Paine. This method compares a target company to the other companies in the same industry with a similar stage of development. Regionality is another criterion in this method as geographic location (i.e., the ecosystem, networking opportunities, and concentration of entrepreneurs and investors) tends to have a big influence on the valuation of startups.

The first step in the Scorecard Valuation Method is to establish the median pre-money valuation for similar pre-revenue startups located in the region where your target company is based. This number will later become the yardstick for the appraisal you will conduct.

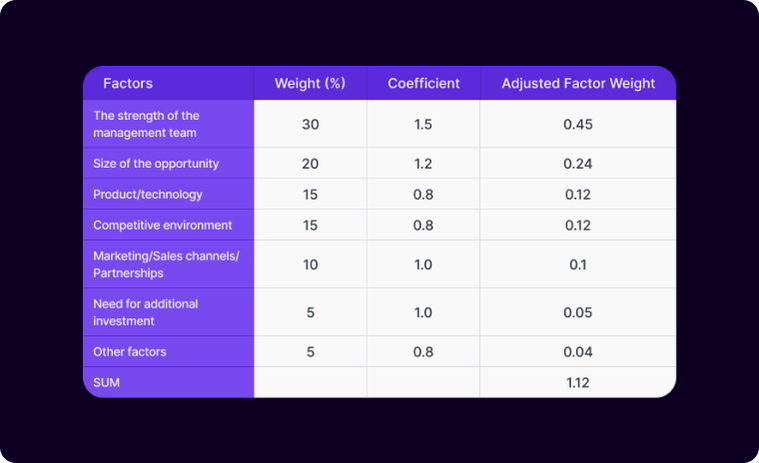

The second step involves a list of factors that guide the appraisal process and the weights you assign to each one of them:

- The strength of the management team (0–30%)

- Size of the opportunity (0–25%)

- Product/technology (0–15%)

- Competitive environment (0–10%)

- Marketing/Sales channels/Partnerships (0–10%)

- Need for additional investment (0–5%)

- Other factors (0–5%)

With the Scorecard Valuation Method, you are basically trying to find out how your company stacks up against the competition. As can be seen from the list above, the method privileges the quality of the management team above everything else, even the product itself. This fact stems from Bill Paine's belief that a good management team can correct early product flaws, while a good product will eventually succumb to bad management.

Assigning weights to each factor is a subjective process, as is the self-assessment you will conduct about your capabilities compared to your competitors. You go through the list of parameters and put a number on how much better or worse you think you are than the average competitor in that particular area. Do you believe that your management team is significantly, like 50 percent, better than your average competitor? Then you can assign a 1.5 coefficient to the first factor. If you think your product isn't at the same level as the rival product and lagging behind by, for example, 20 percent, your coefficient for the third factor is 0.8. A coefficient of 1.0 denotes that the startup matches the industry average in that factor. Let's take a look at an example to see how this works:

This example takes a hypothetical company with a management team that is 50 percent more effective than the rivals. The founder assesses that the opportunity he is looking at is 20 percent bigger than what his rivals are looking at, while his product is not at the same level as the competing products. The startup is in a harsh competitive environment; hence, the 0.8 coefficient for both the product and the competitive environment factors. The marketing team and the need for additional investment are on par with the competitors, and the influence of other factors is 80 percent of what it is for rival companies.

The sum of factors in this example is 1.12, meaning the startup in question is 12 percent more valuable than the median valuation of the startups in the region. So, if the median valuation is $3 million, our startup is worth $3.36 million. This method involves a lot of qualitative judgment in deciding the weights of different factors and how the startup stacks up against the competition in each of them. But, the result is as good as any valuation in the absence of financials and prior investment.

Cost-to-duplicate Method

Pre-revenue micro SaaS startups are like the rookies of the startup world: They are difficult to read. They have no recurring revenue that a potential buyer can use as a base for valuation. Their metrics are sparse and, most of the time, meaningless. The product features may imply high potential, but there is too little body of work to justify a lucrative offer. When it is difficult for a micro SaaS startup founder or a prospective buyer to implement the Berkus Method or the Standard Valuation Method for whatever reason, one has to make do with what is available. The Cost-to-duplicate Method is the last resort founders and investors can use when nothing else works.

The Cost-to-duplicate Method is based on appraising the value of a startup's physical assets, real estate, and inventory to determine how much it would cost for an investor to build the same company. For a software startup, the valuation would be based on the cost of the engineering hours spent on the product because these companies have no inventories or capital investments in real estate or machinery.

The Cost-to-duplicate Method has two disadvantages: It does not factor in things like intellectual property, brand value, or the growth potential of the startup, and it does not work with older startups as more projects are considered failures after a few years without traction. This particular method gives us a "lowest acceptable offer," a base price to use during negotiations. It helps founders salvage some value from a project they would otherwise quit and serves as a nice fallback plan for a project that did not gain any traction.

Conclusion

Founders of micro SaaS startups are in this game for the long run. Their primary areas of focus are bonding with their customer base and nurturing their loyalty. In the meantime, a founder should also be ready for an exit right from day one. That requires coming up with a sensible valuation for the startup.

Micro SaaS startups do not easily lend themselves to traditional appraisal methods. However, "when there is a will, there is a way," as they say. With a little bit of creativity and the three methods listed above, micro SaaS appraisal is no longer the hurdle it might seem to be at first.

Please

fill out this field

Please

fill out this field